.png)

Fast-to-market tech with access to rich data that informs decisions and opportunities

Fast-to-market tech with access to rich data that informs decisions and opportunities

A bank-branded, all-in-one interface that saves SMEs time and makes their lives easier

Marketing and engagement services that increase SME awareness and uptake

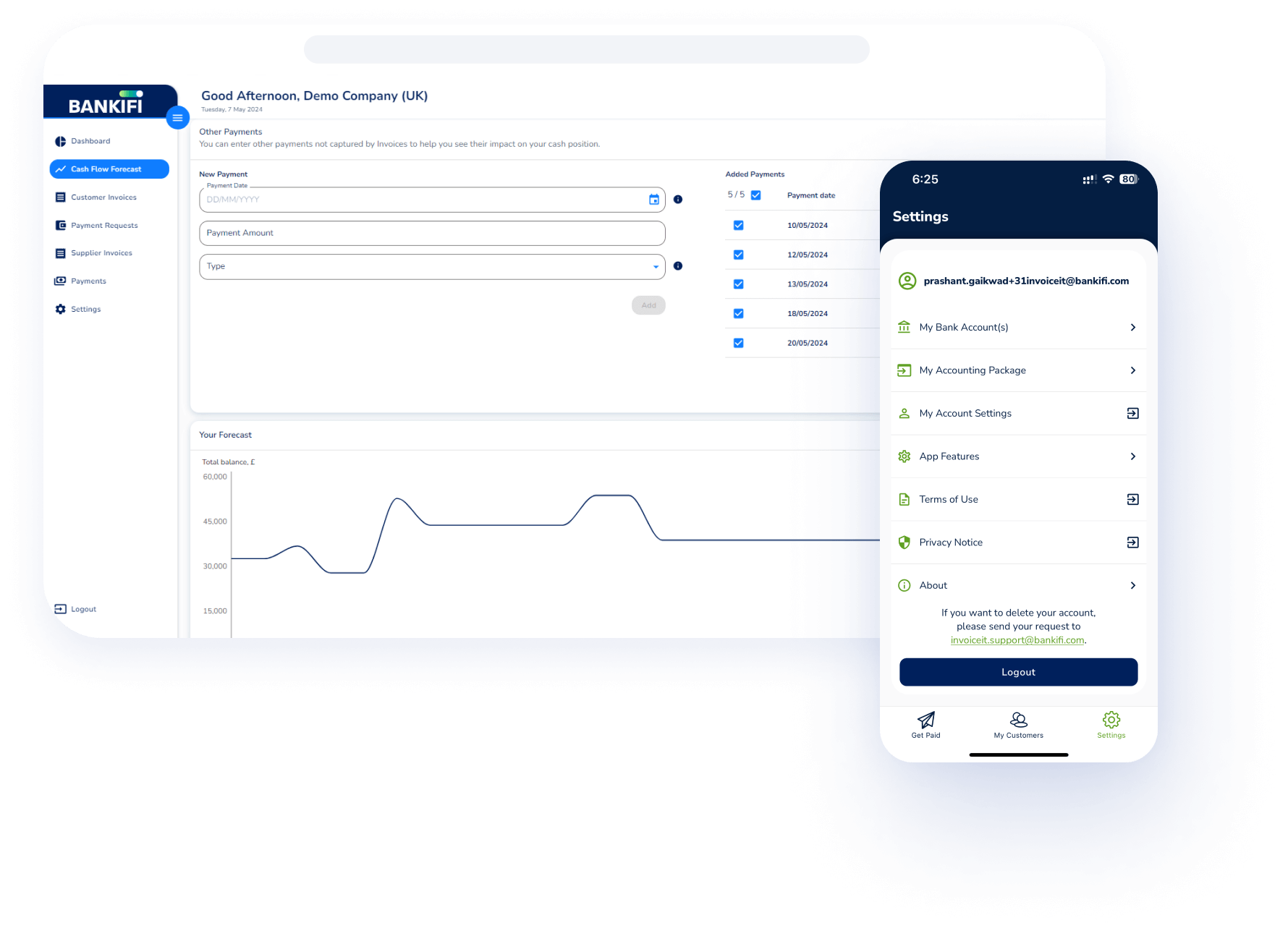

Transform traditional banking experiences into dynamic, interactive and customer-focused interactions. See BankiFi’s tech in action.

.png?width=600&name=Rectangle%20316%20(3).png)

From the innovative core banking technology to the marketing and engagement services that bring it all together, we’ve got it covered.

We’re focused on helping banks transform their relationships with small businesses. Uncover what we mean by engagement banking as a service.