.png)

Time to focus on the SME – embracing your business customers - the way they want – through your bank

The debate around Open Banking and its opportunities tends to go in two directions: the FinTech unicorns, a dialogue fuelled by the fintech community itself and the investors buzzing around the space and on the other hand, ‘Who will survive?’ the bank versus fintech/bigtech debate. Surprisingly the customer, despite age long expressions of customer centricity does not feature in either very prominently. And if one dives deeper, beyond the consumer level very little, by comparison, is heard.

A recent – very thoroughly researched – infographic by Fortunly aptly shows the disrupters and their impact on the financial services industry. A lot of the facts point to the fintech for consumer space, but it also demonstrates that the digitally oriented part of the SME community (25% of global total) is ready for open banking. 89% are willing to share data when it produces a relevant response, 56% use fintech services for banking and payments and 46% look – not surprisingly – outside the bank for their financing requirements.

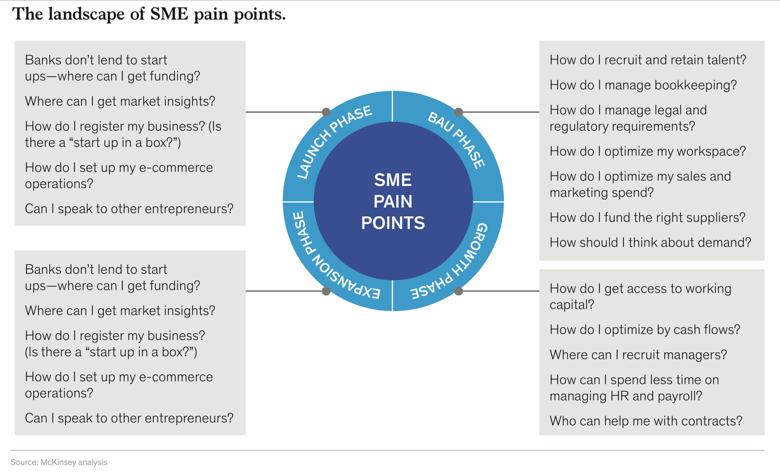

A few very good reports came out around SME opportunities, primarily by the large consulting partners such as KPMG and Accenture, a paper by ATKearny and this summer an in-depth report by McKinsey. All of the above have a few things in common:

- The SME community feels hugely underserved by the traditional banks

- Entrepreneurs want to focus on their core business and see administration as a necessary hazard, best performed in half an hour a day at the breakfast table.

- Nice fintech apps jump in the fray to solve payments and receivables and in particular lending needs.

Banks are considering fintech collaboration to address all of the above ranging from a redirect to the bank Appstore up to orchestration and hard integration with fintechs or even build.

And yes, we see SME focused neo-banks popping up such as Coconut and Tide in the UK. We see accounting package providers marching into the banks’ space by applying for payments licenses, fintech app providers seeking closer cooperation with banks and vice versa. Rabobank in the Netherlands launched an interesting proposition this week which is an example of the latter: Bizzy: full service SME banking and administration through a close link with Tellow (only in Dutch I am afraid).

So where does this leave the incumbent banks

There are many reasons why the existing banks can play a big role in the ‘coming to the rescue’ of the entrepreneurial part of our society, who are in fact, the backbone of our economy. Also, SMEs represent no less than 850 bn of banks’ revenue as per the ‘Beyond Banking’ report with an approximate growth of 7% over the next seven years. That alone should be a good reason in an environment where ‘money talks’. But there is more. Banks already serve those customers, not to their satisfaction but still in many cases as their primary bank account. This means an addressable market, albeit with a limited time span of opportunity.

Furthermore, we might not love our banks, but all research shows that we do trust them, and we know they are very tightly regulated and are at least doing a lot to protect our privacy. The actions around the use of data by many large tech firms that have become public lately, do not instil a great deal of confidence in the ‘new players’ being any more caring or careful than the banks we know.

Will all banks get it? Well depending on how we define ‘all’ and ‘it’, that is yet to be seen, but let’s take a look at what banks can do in the new open banking world, where none controls the outcome. Let’s take just three angles, that are totally within reach and possibility:

- Activate the decade long promise of Business Customer Centricity

- Bite back at the intruders by doing better

- Embrace the reality and be brave

Business Customer Centricity

When you ask a banker – or to be fair – a technology provider - what business customers want the discussion immediately jumps to functionality, product features and processes. Wrong. A business owner is a person, who feels, thinks and acts like a human. He or she instinctively will feel accepted, safe or just ok with your bank. He will think about the service offering and compare it to others before coming on board. And he will act like any human when it comes to referring you to others when things are great, remaining a customer when he feels rewarded for his loyalty or leaving when he or she feels neglected.

This triangle of feel, think and act is what opens, builds and cements a relationship, not just features. Customers will perceive this full circle more when on top of this you offer relevance that fits around their life, not yours. Breaking down the product silos is not a luxury; it is a prerequisite for success. From product to service is the way to their heart and business.

So as businesses go through the life stages of starting up, building the business, growing the business, expanding or even selling off the business, you as a bank can be the partner of choice by offering the right level of service at the right price with maximum flexibility and responsiveness at every stage.

The good news for the bank is that with today’s (cloud based) technology you can offer this at the right cost level too. And finally, a business customer acquired at the earliest stage is a ‘low cost’ acquisition that might lead to a business and private banking customer for life.

Up your game by doing better than the ‘intruders’

The number one reason why many businesses turn to fintech suppliers for accounting, payments and banking services is because the nimble tech players connect processes into a logical flow of actions around the entrepreneur’s life. Businesses want to spend most of their time on core business (acquiring new customers and serving existing ones) and secondary be compliant, professional and in control when it comes to all non-core ‘stuff’.

Making and sending invoices and getting paid today means ‘hopping’ between an accounting package (or excel sheet) and a digital banking environment. Chasing outstanding money is a matter of the accounting package, the digital banking overview, a phone and or email. Paying taxes requires calendar alerts, one eye on cash flow and the other on the VAT amounts on invoices, receipts etc.

Accounting package providers have seen this coming for a long time and embrace PSD2 for they can apply for a payments license and thus creep into the bank’s relationship with the business. Why would you let them? And no, the answer is not just opening an API to any package provider. Go beyond and bring accounting into your bank account. Go bank account-ing and be the platform: the portal your business customer refers to for any task. Be the go-to ‘person’ you promise you are. In a world where we are at risk of wandering around clueless in a jungle of apps, the last thing an entrepreneur needs is a journey from bank to – more or less – connected app – and full circle back again. A bank Appstore is not a bad idea at all, but when it comes to the core of your customer relationship you can bring this app-style tech as a micro business service inside your own reach and domain. The customer happy for he knows the channel of his or her choice by now and the bank gets very direct insight to serve his customer even better when it comes to financing, forex, etc.

In the face of reality: be brave

Being brave in the face of reality rings very differently in peace times than in times of terror, war or personal threat. Banks with a zest for innovation also need to take a good look at reality first and then assume a brave attitude.

There is very little point in guessing outcomes when faced with complexity, there is even less point in building a plan based on wild assumptions. It has been said before, in terms of Open Banking, we are crossing the Rubicon. Players, adoption rates, pricing models are all undefined to a large degree.

What does make the difference for any company is being brave in the light of the chosen approach. This change in society is not regulatory, technological nor incremental. It is a fundamental shift and as such a relatively equal playing field. Five years ago, Forbes published a great article on Brave Innovation: study your environment, as unclear as it might be. Know your own value system and align it with your attitude and behaviour. Choose your partners wisely, but mostly very complimentary. Don’t compete for superior knowledge or expertise, understand and trust each other’s skill sets. And most of all study the impact of your endeavours on your customers, get under their skin, listen and learn. Oh, and very unlike banks: customers do not expect perfection on day one, but something that is simple and relevant. Go for an MVP, launch, listen, adapt and scale rapidly.

Be brave, it is time to make your business customers experience your bank – they are ready for it.

More on ‘Trusting the Cloud’ in our next blog and why you can, explained in laymen’s language.

.png?width=600&name=Rectangle%20316%20(3).png)